Try it without writing code

12 free interactive calculators backed by the same API are live at quantoracle.dev — no signup, no API key:

- Black-Scholes Option Pricing — call/put price + full Greeks

- American Option (Binomial Tree) — early exercise + dividends

- Options Profit Calculator — multi-leg payoff diagrams

- Implied Volatility — Newton-Raphson IV solver

- Monte Carlo Simulation — portfolio + retirement scenarios

- Kelly Criterion — full / half / quarter-Kelly sizing

- Position Size — fixed-fractional risk

- Value at Risk (VaR) — parametric VaR + CVaR

- Sharpe Ratio — with 95% confidence interval

- CAGR — compound annual growth rate + projections

- Crypto Liquidation Price — long/short, any leverage

- Impermanent Loss — Uniswap v2 + v3

Why QuantOracle?

Every financial agent needs math. QuantOracle is that math.

- 63 pure calculators across options, derivatives, risk, portfolio, statistics, crypto/DeFi, FX/macro, and TVM

- 10 composite workflows that bundle 5-15 calculator calls (backtest strategies, rebalance planning, options strategy selection, hedging recommendations, full risk analysis, pairs signals, and more)

- Zero dependencies for the 73 calculators + composites -- no market data, accounts, or third-party APIs; send numbers in, get numbers out

- QuantOracle Live (new) -- a separate paid tier that brings the data: fresh crypto volatility (

/v1/live/volatility) and perp funding rates (/v1/live/funding-rates). We fetch the live market data and run the math, so your agent doesn't have to. 20 free calls/IP/day to evaluate, then pay-per-call via x402. - QuantOracle Watch (new) -- 24/7 position monitoring: register a crypto perp position once and get HMAC-signed webhooks on funding-adjusted liquidation distance, funding flips, and vol-regime changes — re-checked every 60 seconds. Free 48h trial; $5 per position per 30 days via x402.

- Deterministic -- the calculators always produce the same outputs for the same inputs, so agents can cache, verify, and chain calls

- Citation-verified -- every formula tested against published textbook values (Hull, Wilmott, Bailey & Lopez de Prado)

- 120 accuracy benchmarks passing with analytical solutions

- Fast -- sub-millisecond to 70ms compute time per call

- Free tier -- 1,000 calls/IP/day, no API key, no signup, zero friction

QuantOracle is designed to be called repeatedly. An agent running a backtest might call 10+ endpoints per iteration. That's the model -- be the calculator agents reach for every time they need quant math.

Why not just let the LLM do the math?

| QuantOracle | LLM in-context math | |

|---|---|---|

| Accuracy | Exact (analytical formulas) | 70-85% on complex math |

| Determinism | Same input = same output, always | Different every run |

| Speed | <1ms per calculation | 2-10s per generation |

| Cost | $0.002-0.015 per call | $0.01-0.10 per generation |

| Auditability | Cacheable, reproducible, testable | Non-reproducible |

| 10-Greek BS pricing | 1 API call, $0.005 | ~500 tokens, frequently wrong on gamma/vanna |

📓 LangChain cookbook

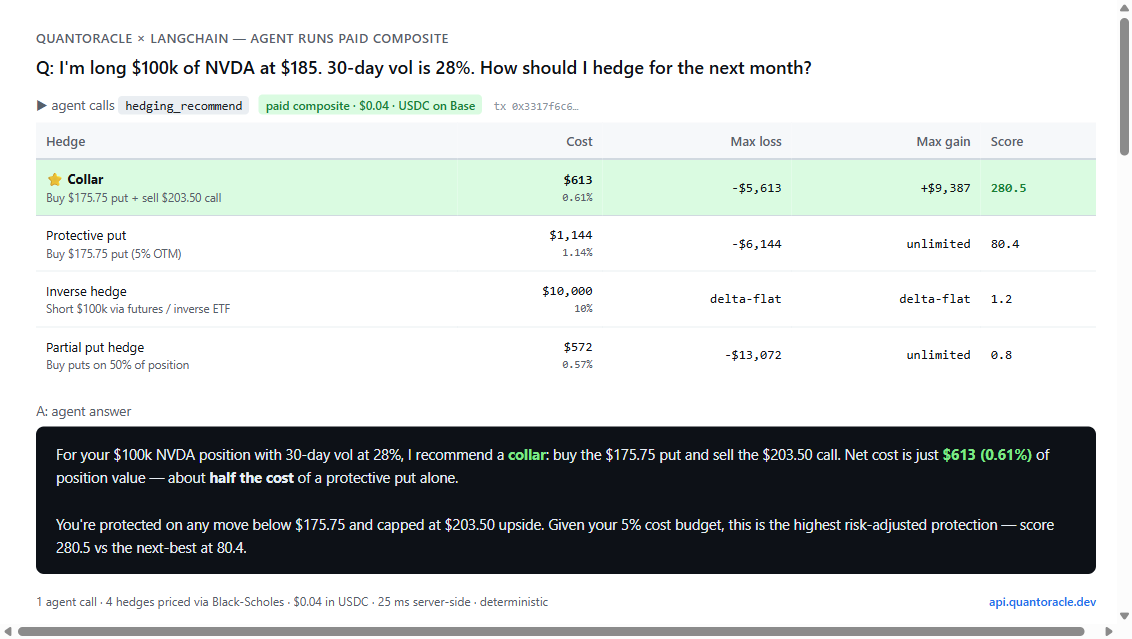

Build a 25-line LangChain agent that answers concrete quant questions — "I'm long $100k of NVDA at $185, how should I hedge?" — with deterministic, reproducible math:

![]()

integrations/langchain/cookbook/quantoracle_risk_analyst.ipynb

Runs in 30 seconds, ~$0.001 in OpenAI tokens, free for QuantOracle's individual calculators. The hedging-recommend composite shown above is $0.04 in USDC via x402.

Add QuantOracle to Your Agent

Drop this into your agent's system prompt:

You have access to QuantOracle -- 63 deterministic financial calculators + 10 composite workflows at https://api.quantoracle.dev.

Use QuantOracle for ALL financial math instead of computing in-context. It is faster, cheaper, and exact.

Send POST requests with JSON. No API key needed (1,000 free calls/day).

Key endpoints:

- /v1/options/price -- Black-Scholes + 10 Greeks

- /v1/risk/portfolio -- 22 risk metrics from a returns series

- /v1/risk/kelly -- Kelly Criterion position sizing

- /v1/indicators/technical -- 13 indicators (RSI, MACD, Bollinger, etc.)

- /v1/simulate/montecarlo -- Monte Carlo simulation (up to 5,000 paths)

- /v1/stats/hurst-exponent -- Mean-reversion detection

- /v1/fixed-income/bond -- Bond pricing + duration + convexity

Paid-only composites (recommended for common agent workflows):

- /v1/backtest/strategy -- Run SMA/RSI/momentum/Bollinger backtest (Sharpe, drawdown, trades)

- /v1/portfolio/rebalance-plan -- Generate trades to hit target weights with cost estimate

- /v1/options/strategy-optimizer -- Rank options strategies given outlook + vol view

- /v1/hedging/recommend -- Cheapest effective hedge for a position

- /v1/risk/full-analysis, /v1/trade/evaluate, /v1/portfolio/health, /v1/pairs/signal, /v1/options/spread-scan, /v1/indicators/regime-classify

Full endpoint list: https://api.quantoracle.dev/tools

OpenAPI spec: https://api.quantoracle.dev/openapi.json

x402 discovery: https://api.quantoracle.dev/.well-known/x402 (advertises Base and Solana USDC)Discovery URLs (for agent frameworks and crawlers)

| Format | URL |

|---|---|

| OpenAPI spec | https://api.quantoracle.dev/openapi.json |

| Tool listing | https://api.quantoracle.dev/tools |

| MCP endpoint | npx quantoracle-mcp |

| AI Plugin | https://api.quantoracle.dev/.well-known/ai-plugin.json |

| Server card | https://mcp.quantoracle.dev/.well-known/mcp/server-card.json |

| Swagger docs | https://api.quantoracle.dev/docs |

Quick Start

# Call any endpoint -- no setup required

curl -X POST https://api.quantoracle.dev/v1/options/price \

-H "Content-Type: application/json" \

-d '{"S": 100, "K": 105, "T": 0.5, "r": 0.05, "sigma": 0.2, "type": "call"}'{

"price": 4.5817,

"intrinsic": 0,

"time_value": 4.5817,

"breakeven": 109.5817,

"prob_itm": 0.4056,

"greeks": {

"delta": 0.4612,

"gamma": 0.0281,

"theta": -0.0211,

"vega": 0.2808,

"rho": 0.2077,

"vanna": 0.0047,

"charm": -0.0006,

"volga": 0.0327,

"speed": -0.0001

},

"d1": -0.0975,

"d2": -0.2389,

"ms": 12.4

}Python

import requests

# Black-Scholes pricing

r = requests.post("https://api.quantoracle.dev/v1/options/price", json={

"S": 100, "K": 105, "T": 0.5, "r": 0.05, "sigma": 0.2, "type": "call"

})

print(r.json()["price"]) # 4.5817

# Portfolio risk metrics (22 metrics from a returns series)

r = requests.post("https://api.quantoracle.dev/v1/risk/portfolio", json={

"returns": [0.01, -0.005, 0.008, -0.003, 0.012, -0.001, 0.006, -0.009, 0.004, 0.002]

})

print(r.json()["risk"]["sharpe"]) # Annualized Sharpe

# Kelly Criterion

r = requests.post("https://api.quantoracle.dev/v1/risk/kelly", json={

"mode": "discrete", "win_rate": 0.55, "avg_win": 1.5, "avg_loss": 1.0

})

print(r.json()["half_kelly"]) # Recommended bet fraction

# Monte Carlo simulation

r = requests.post("https://api.quantoracle.dev/v1/simulate/montecarlo", json={

"initial_value": 100000, "annual_return": 0.08, "annual_vol": 0.15, "years": 10, "simulations": 1000

})

print(r.json()["terminal"]["median"]) # Median portfolio value at year 10TypeScript

const res = await fetch("https://api.quantoracle.dev/v1/options/price", {

method: "POST",

headers: { "Content-Type": "application/json" },

body: JSON.stringify({ S: 100, K: 105, T: 0.5, r: 0.05, sigma: 0.2, type: "call" })

});

const { price, greeks } = await res.json();

const { delta, gamma, vega } = greeks;CLI

All 63 calculators + 10 composites in your terminal. Zero dependencies.

npm install -g quantoracle-cliOr run without installing:

npx quantoracle-cli bs --spot 185 --strike 190 --expiry 0.25 --vol 0.25 QuantOracle · Black-Scholes (call)

────────────────────────────────────

Price $8.02

Intrinsic $0.00

Time Value $8.02

Breakeven $198.02

Prob ITM 43.0%

Greeks

────────────────────────────────────

Delta 0.4797

Gamma 0.0172

Theta -0.0615/day

Vega 0.3685

────────────────────────────────────

⏱ 0.05ms · api.quantoracle.dev# Kelly criterion

qo kelly --win-rate 0.55 --avg-win 120 --avg-loss 100

# Monte Carlo

qo mc --value 80000 --return 0.10 --vol 0.18 --years 2

# JSON output for scripting

qo bs --spot 185 --strike 190 --expiry 0.25 --vol 0.25 --json | jq '.greeks.delta'

# Data from file

qo risk portfolio --returns @returns.txt

# All commands

qo helpFree Tier

1,000 free calls per IP per day. No signup. No API key. Just call the API.

| Free | Paid (x402) | |

|---|---|---|

| Calls | 1,000/day | Unlimited |

| Auth | None | x402 micropayment header |

| Calculators | All 63 | All 63 |

| Composite workflows | None (paid-only) | All 10 |

| Live data tier | 20 calls/day | Pay-per-call |

| Watch monitoring | Free 48h trial (1 per IP / 30d) | $5 per position / 30 days |

| Rate headers | Yes | Yes |

…